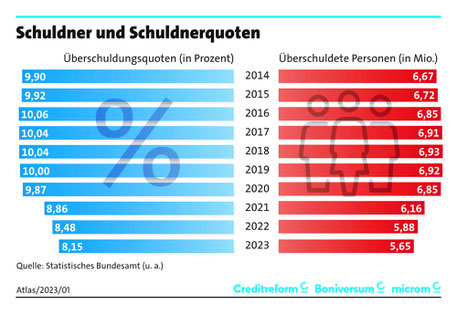

5.65 million citizens over-indebted / “hidden increase” in over-indebtedness / over-indebtedness ratio of 8.15 percent / trend reversal due to persistent inflation and high interest rates / recession as a driver of over-indebtedness

The over-indebtedness situation of consumers is ambivalent. At first glance, it has improved slightly again in 2023. Only 5.65 million people (-233,000 cases compared to the previous year) will be considered over-indebted in Germany in 2023. Officially, this is another low. The over-indebtedness rate, i.e. the proportion of over-indebted people in relation to all adults in Germany, fell by 0.33 points to 8.15 percent.

“Hidden trend reversal”

“The supposedly good values are unfortunately deceptive,” says Patrik-Ludwig Hantzsch, head of economic research at Creditreform. “Without special statistical effects, we are measuring an increase in over-indebtedness for the first time since 2019.” The background is a shortening of the storage periods for residual debt relief from the previous three years to now six months. According to the old reading, there are around 17,000 more cases than in 2022. The over-indebtedness rate would actually be 8.51 percent, slightly higher than the previous year. Since 2020, with the start of the Corona crisis, cases of over-indebtedness have fallen dramatically. Government aid and a strong willingness to save protected many consumers. “The multiple crises, especially persistent inflation and high interest rates, are constantly making consumers’ lives more expensive,” continued Hantzsch. “Citizens' desire to consume is growing again, even though almost everything is significantly more expensive. This will financially overwhelm many people.” Since the consequences of excessive indebtedness, such as personal insolvency, only appear with a delay, analysts expect the number of cases to increase in the coming months.

Stable situation, mixed prospects

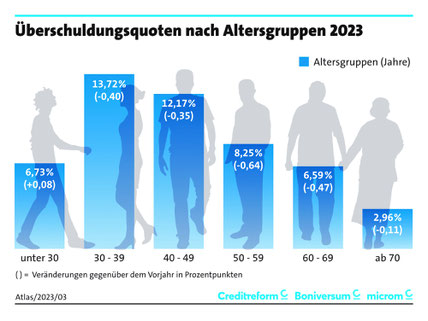

In addition to the “hidden trend reversal,” other parameters also change. “We are observing that so-called “soft” over-indebtedness, i.e. sustained payment disruptions, is increasing again for the first time since 2020,” explains Michael Goy-Yun, Managing Director of Creditreform Boniversum and microm. “Dramatic increases in living and energy costs have significantly limited consumers’ financial flexibility in the last year.” The so-called “permanently over-indebted” people from lower social classes in particular suffered from the price development. “The increasing demand for installment loans and “buy now, pay later” offers, which are primarily aimed at younger people and women, confirm the consumer trend,” Goy-Yun continued. It is also these two groups where the “soft” over-indebtedness is increasing against the trend. “In the youngest age cohort (up to 29 years of age), there is actually an increase in cases of over-indebtedness and the overall rate for the first time since 2013. Those over 70 years of age recorded the smallest decline in the over-indebtedness rate. However, in the long term, the development of the age groups is the opposite. While young people in particular (under 30 years of age) have become increasingly less over-indebted over the past 10 years, the over-indebtedness rate of those over 60 years of age has increased significantly over the same period.

“It is also striking,” says expert Goy-Yun, “that low-income households continue to be most affected by over-indebtedness. But if we look at the crisis years since 2019, we see that this group has obviously benefited greatly from the state's support measures." Their share of overtraining fell by 5 percentage points, while more normal and high earners (in total + 5 percentage points) in have fallen into a spiral of over-indebtedness and some have sought debt advice. “Specifically, these could be people whose real estate financing is expiring in this interest rate environment, who need follow-up financing and suddenly have to cope with enormous additional financial burdens,” explains Goy-Yun.

Recession as a driver of excessive indebtedness

“The state’s numerous measures have significantly relieved the burden on the lower income groups in particular. It is questionable whether the aid will have a long-term effect,” said economic expert Hantzsch. “The sharp increase in the minimum wage in 2022 and the citizen's allowance, for example, have provided relief for the moment, but the price for this is particularly high for the small-scale economy, as their wage costs rise in the long term and personnel-intensive industries find fewer employees,” continued Hantzsch. “Consumer over-indebtedness is closely linked to economic developments. The economic prospects are uncertain, but bleak across the board,” said Hantzsch. “The trend in corporate insolvencies has already begun to reverse.” The impact on consumers is only a matter of time, since, for example, the situation on the labor market is getting worse again despite demographic change and Germany is in the last places in terms of growth. “If manufacturing companies turn their backs on Germany as a business location, it will cost well-paid jobs and the financial security of employees,” said Hantzsch.

Country trends remain positive

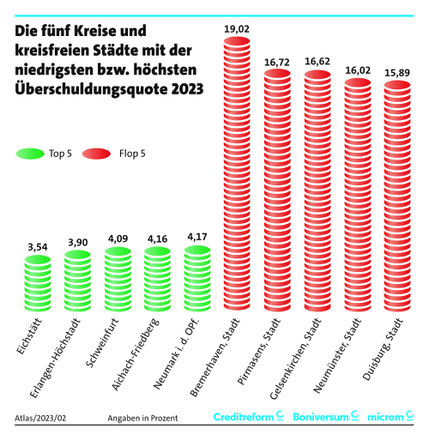

The number of cases of over-indebtedness also fell to a similar level in both parts of Germany in 2023 - although not as sharply as in previous years. Both parts are in the light green area of the over-indebtedness traffic light. In the current year, 394 districts and independent cities in Germany (98.5 percent) showed a decrease in the over-indebtedness rate. Here too, the analysis shows that soft over-indebtedness is on the rise: in more than half of all districts and independent cities in Germany (57 percent) the soft over-indebtedness rate has increased.

Source: Creditreform

Write a comment