A number of Debtsource clients have over the past months queried with us what the difference is between a surety and guarantee. In some cases clients prefer to have a surety, while other clients are advised by their legal representatives to rather call for an unconditional guarantee.

Credit Guarantee Insurance Corporation (CGIC) recently circulated a memo on the differences between the two forms of security, and for those interested in the technical aspects of B2B credit securities, the document provides good guidance on which document should be used when.

Suretyships

A suretyship is an accessory contract to another contract in terms of which a surety binds himself as a debtor to the creditor of another person (the principal debtor) to render the whole or part of the performance due to the creditor by the principal debtor, if and to the extent that the principal debtor fails, without excuse to render the performance himself.

Accessory means that a surety’s liability is accessory to that of the principal debtor and the surety effectively undertakes primarily that the principal debtor will perform, and secondarily that he, the surety, will perform if the principal debtor fails to do so.

The addition of the words “co-principal debtor” in a suretyship does not transform the contract into any contract other than one of suretyship.

Guarantees

Contracts of guarantee create primary obligations that are not dependent upon the existence of any other debt. What this means is that in terms of a contract of guarantee, the guarantor undertakes a principal obligation to indemnify a creditor on the happening of specified events.

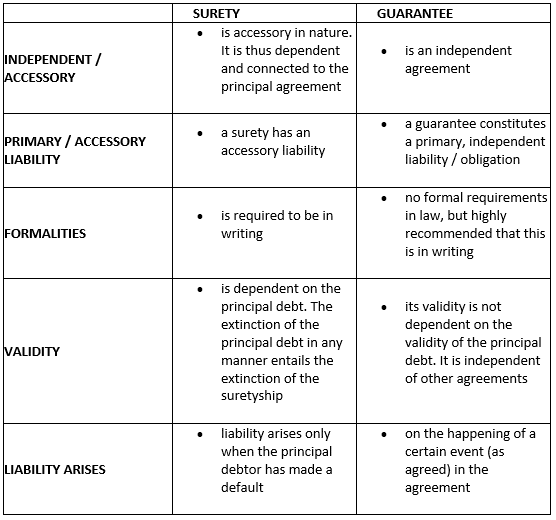

The difference between a surety and guarantee is tabled below:

For those who wish to better understand securities, be sure to attend our upcoming virtual Debtsource Academy to be held in May.

Source: Debtsource

Write a comment